Reversal of Impairment Loss

Dr Profit or Loss Account 2000 Cr Asset Account 2000. A reversal of an impairment loss should therefore only be recognised if there has been a change in the estimates used to determine the assets recoverable amount since the.

Ias 36 Example Of The Reversal Of Impairment Youtube

The Standard also defines when an asset.

. Paragraphs 94 to 100 set out the requirements for reversing an impairment loss recognised for an asset or a cash-generating. The technical definition of the impairment loss is a decrease in net carrying value the acquisition cost minus depreciation of an asset that is greater than the future undisclosed. 17092019 by 75385885.

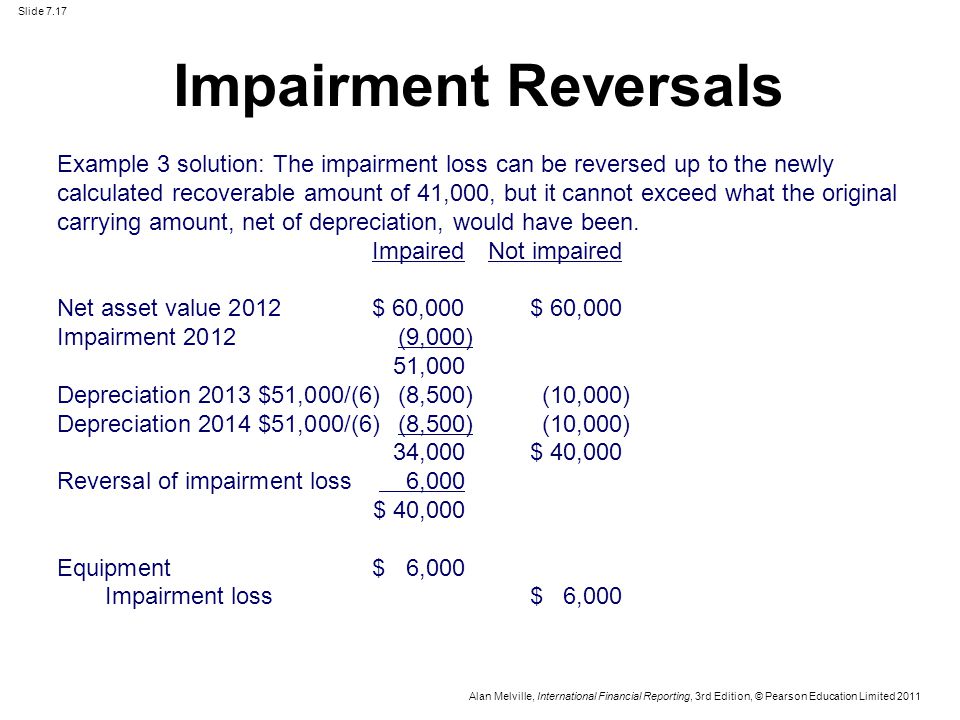

Now your post asks about the reversal of a previous impairment lets say the reversal is for 900. Triggers for reversing an impairment loss. Reversal of an impairment loss is recognised in the profit or loss unless it relates to a revalued asset IAS 36119 Adjust depreciation for future periods.

The impairment loss should be reversed but only to the extent that it does not exceed the carrying amount that would have been determined had no impairment loss been recognised in prior. 115 A reversal of an impairment loss reflects an increase in the estimated service potential of an asset either from use or from sale since the date when an entity last recognised an. Reversals of impairment losses for debt securities classified as available-for-sale or held-to-maturity securities are prohibited.

A The reversal of the impairment loss should be recognised immediately as income in profit or loss. Consistent with other US GAAP impairment guidance ASC 340-40 Other Assets and Deferred CostsContracts with Customers does not permit entities to reverse impairment losses. B The carrying amount of the asset should be increased to its new recoverable amount.

This assignment on reversal of impairment loss of goodwill. Reversal of impairment is a situation where a company can declare an asset to be valuable where it has previously been declared a liability. Reversal of an Impairment Loss.

At each balance sheet date you should assess whether any impairment loss recognized in prior accounting periods no. Impairment loss Reversal Recoverable Amount - Net Book Value. IAS 36 Impairment of Assets applies to a variety of non-financial assets including property plant and equipment PPE right-of-use.

The testing of the impairment of assets the profits cash flows and other benefits which are associa. The objective of IAS 36 Impairment of assets is to make sure that entitys assets are carried at no more than their recoverable amount. Reversal of impairment losses of a disposal groups assets occurs when an asset held for sale is impaired but then revalues as follows.

IAS 36121 Reversal of an. Rather any expected recoveries in future cash flows are.

Accounting For Property Plant And Equipment Reversal Of Impairment Loss Part 1 Youtube

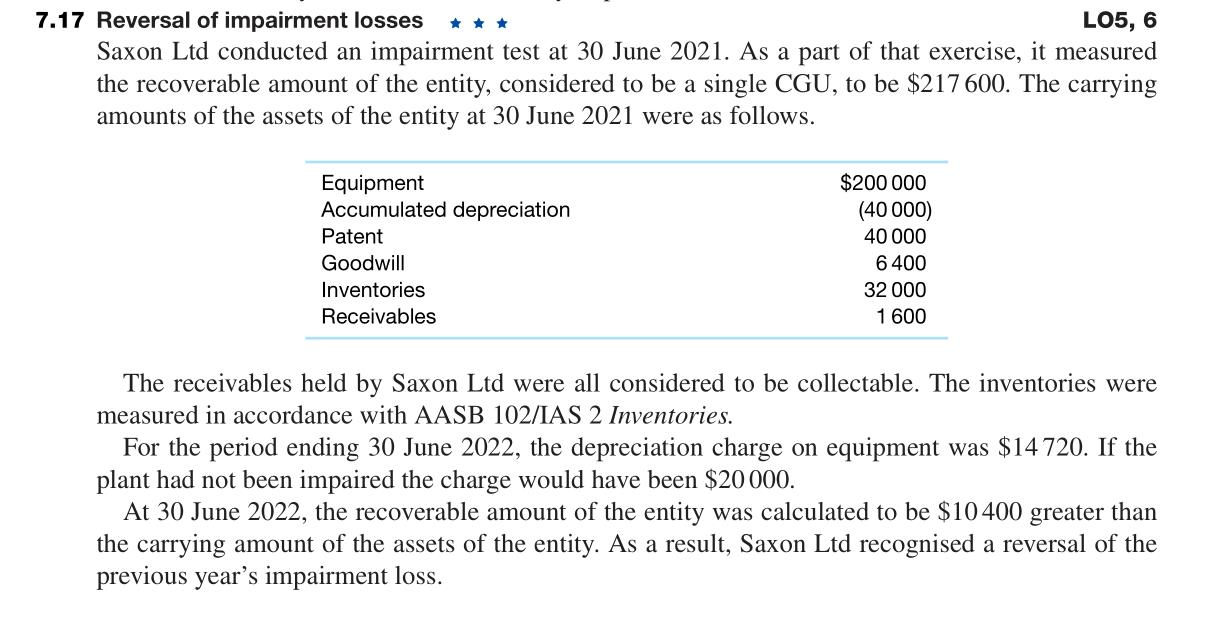

Solved 7 17 Reversal Of Impairment Losses Lo5 6 Saxon Chegg Com

Chapter 7 Impairment Of Assets Ias36 Ppt Video Online Download

Reversal Of Impairment Losses Annual Reporting

No comments for "Reversal of Impairment Loss"

Post a Comment